Future aggregate demand variables to consider

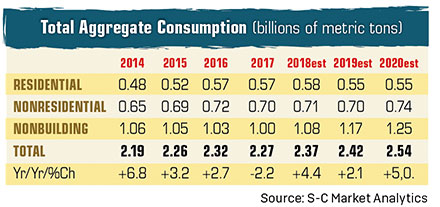

Note: There is a small difference between our estimates of consumption and the USGS because of our own estimates in states where USGS does not report values due to competitive concerns. Click to enlarge.

While the U.S. economy is growing rapidly, construction activity is flatlining.

Private construction demand is down year-over-year as public works continues to grow. We expect private construction to resume growth toward the end of 2019 and into 2020 as low interest rates and continued income growth provide the strength for spending increases.

With the economy growing at close to 3 percent per year, state and local revenues are increasing and have been for more than five years. This increased tax revenue will be spent on higher pension and health care costs, but enough will be left over to fund more infrastructure spending.

The new talks in Washington about a $2 trillion infrastructure bill are encouraging, but, as usual, talks become divisive when it comes time to decide how to pay for a bill.

Regionally, strength remains in the Sun Belt and energy states. For the most part, these are low-cost, low-tax areas that draw in new people regardless of energy activity.

Because the high-tax states do not seem to be reforming their high-tax status, the loss from out-migration will increase for the next few years. Luckily, the strength in the overall economy will mask their problems for a while.

The canary in the coal mine will be local real estate prices. How much they fall will tell us how much they need to reform their tax burdens.

As a result of these changes, construction materials demand will continue to increase for the next few years. Most of the gains will come from the nonbuilding segment, to be joined post-2019 by the private segments (i.e., residential, nonresidential).

Subscribe to Pit & Quarry

If you enjoyed this article, subscribe to Pit & Quarry to receive more articles just like it.