2019: The ‘show me’ year

Growth through acquisition has been the method of choice for top aggregate producers lately, with many large transactions providing acquirers with the ability to expand market share and improve financial performance. Photo: iStock.com/peuceta

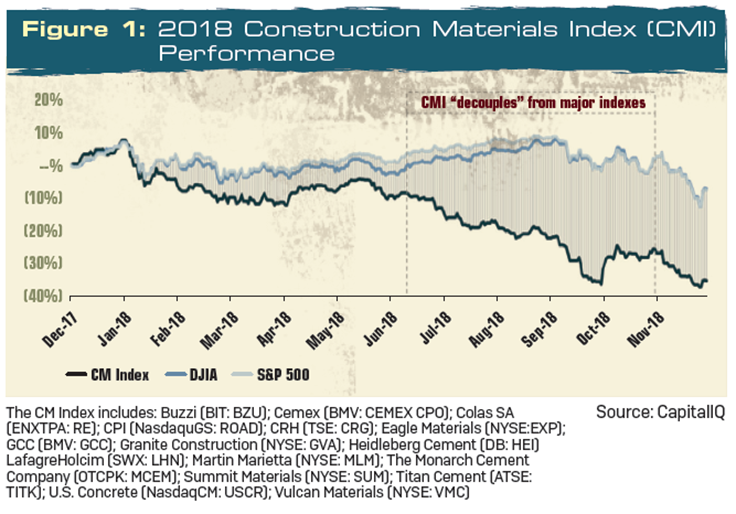

2018 was a year of two halves for the construction materials sector.

The year started with great optimism following a strong 2017, newly enacted tax legislation and the anticipation of infrastructure legislation. As a result, construction materials stocks performed well early in 2018, and analysts expected another record year.

However, as infrastructure legislation failed to gain momentum, interest rates rose, adverse weather affected operations across the country and investors began to lose adverse confidence in sector growth. By late December, FMI’s Construction Materials Index (CMI) was down more than 35 percent for the year, ultimately falling to levels not seen since the first quarter of 2016.

Valuation multiples fell in tandem with stock prices. The CMI median enterprise value to EBITDA ratio (EV/EBITDA) peaked at 11.0x EBITDA in June, bottomed out during the holiday market lows at 7.6x, and has recovered to a median of 9.0x as of late February. Falling EV/EBITDA multiples are often a signal that investors are concerned about future earnings growth rates.

2019 drivers

While the sector did not perform as initially expected in 2018, investor pessimism does not necessarily square with company performance. As CMI companies report 2018 earnings, several key trends have emerged that bode well for 2019:

1. Revenues improved in 2018. CMI firms headquartered in the United States all posted strong growth in revenues for 2018, with Construction Partners Inc., Eagle Materials, Granite Construction and Vulcan Materials each reporting double-digit percentage growth in revenues.

2. Backlogs are strong. CMI companies reported strong demand headed into 2019, with many firms noting the growth in demand from the highway sector. California, Texas, North Carolina, Florida and Georgia, among others, are increasing overall volumes of public lettings.

3. Pricing is improving. Martin Marietta, Vulcan Materials, Summit Materials and others all reported pricing growth in 2018, particularly in aggregate segments. Many are also projecting price increases in 2019.

4. Increased input costs are being passed through. Input costs rose in 2018, particularly for asphalt businesses, but CMI firms have confidence that the current competitive environment allows them to pass these cost increases on to consumers.

High expectations for 2019

Based on this dichotomy of a relatively strong outlook for 2019 and the investor skepticism that dominated for the latter half of 2018, FMI has dubbed 2019 the “show me” year for the construction materials sector. While 2018 was not the year many expected it to be, it was disappointing largely due to factors out of management control – poor weather in the first two quarters of 2018, infrastructure legislation that again failed to pass Congress, increases in interest rates, and trade war discussions, among other factors.

In 2019, investors want proof that weather in 2018 was an anomaly, that highway funding can drive additional growth in volumes, and that the demise of the housing market is overstated. There will be enormous pressure on CMI companies to perform. Analyst expectations are high for 2019.

With pressure to perform, firms have two growth options: organically through existing operations or through acquisition. Over the past few years, the latter has been the growth option of choice, with many large transactions (Martin Marietta-Bluegrass Materials, Vulcan Materials-Aggregates USA; CRH-Ash Grove Cement) providing acquirers with the ability to expand market share and improve financial performance.

2019 will be different. Traditional acquirers are under more pressure to right size balance sheets and grow organically. Still, organic growth can often be challenging. Barriers to entry create many obstacles for market expansion and increasing share.

Thus, if housing and infrastructure spending does not develop as anticipated, CMI companies may turn to the mergers and acquisition market to augment the lack of organic growth opportunities.

M&A activity

What does this mean for mergers and acquisitions (M&A) in 2019? Sellers will need to demonstrate to buyers a compelling value proposition beyond the simple addition of profit. In other words, synergies will drive much of the activity in 2019, bringing smaller bolt-on or regional transactions into focus and likely placing larger transactions (which often require substantial amounts of debt to finance) under more scrutiny.

However, sellers with leading market positions and strong growth profiles will always gain attention, particularly from several CMI firms that have returned to the M&A market after a multi-year hiatus.

Lastly, buyers and investors broadly will be focused on when the next recession will occur. Regardless of when it does occur, the long-term outlook for the construction materials sector remains healthy, with several catalysts that could accelerate both volumes and profitability.

Federal infrastructure spending will top the list of highly watched developments in 2019, with interest rates, housing markets and other potential global developments also taking on critical importance.

In sum, optimism for 2019 is warranted. But those looking to execute a transaction will need to demonstrate increases in revenue and profitability to achieve full value – a “show me” year, indeed.

George Reddin, managing director, and Scott Duncan, director, are with FMI Capital Advisors Inc., FMI Corp.’s investment banking subsidiary. They specialize in mergers and acquisitions and financial advisory services.

Subscribe to Pit & Quarry

If you enjoyed this article, subscribe to Pit & Quarry to receive more articles just like it.