The latest merger & acquisition influencers

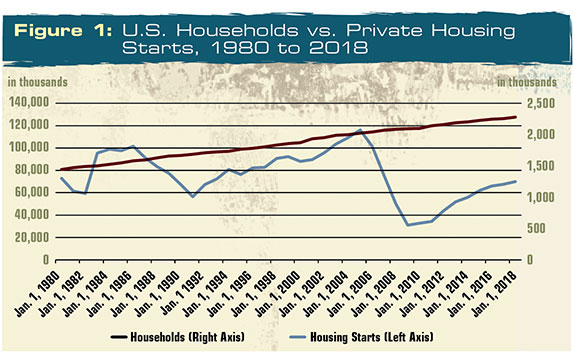

While U.S. households have steadily grown over the last 40 years, housing starts have experienced some turmoil – particularly in the mid-2000 period. Source: FMI. Click to enlarge

If headlines are any metric, there is ample reason to be concerned about an emerging recession in the United States.

In August, the two-year treasury yield exceeded the 10-year yield (often an early sign of recession), and in September tariffs on more than $112 billion in Chinese goods took effect. Housing prices and starts, meanwhile, appear to have leveled off and even declined somewhat versus prior years.

Each of these developments is driving dire headlines in the financial media and increased uncertainty in a growth cycle that is already historic in its duration.

CMI performance

Despite these developments, the performance of public construction materials companies remains positive. Most of FMI’s Construction Materials Index (CMI) firms reported gains in both volume and pricing in the U.S. during the second quarter, with wet weather being one sticking point for many producers.

Of FMI’s CMI firms, GCC, Martin Marietta and Vulcan Materials all exceeded analysts’ revenue expectations, and Cemex, CPI and Vulcan exceeded expectations for second-quarter GAAP (generally accepted accounting principles) earnings per share. Nearly every company with the CMI indicated that weather disrupted their second-quarter performance, increasing pressure on companies to regain lost volume in the second half of 2019.

M&A activity

In addition, the market for mergers and acquisitions (M&A) continues to be active, with many sellers in the market. Still, relatively few deals are closing compared to what was a busy first half of 2018.

The juxtaposition of sellers’ strong financial performance with the potential for a recession over the course of the next 12 to 24 months has made transaction pricing increasingly difficult. Sellers want their business valued on recent performance, while buyers always look to the future.

The effect of weather on public companies’ income statements has also made larger transactions increasingly difficult to finance. This dynamic is leading many buyers to be more selective and to focus on smaller to mid-sized transactions with clear synergy opportunities.

Other indicators

Despite the view that a recession is inevitable, there is reason to remain positive on the construction materials sector. The two critical drivers of construction materials volumes – residential construction (housing) and highway construction (infrastructure) – remain fundamentally strong.

Annual production of new homes, a key driver of ready-mix, aggregate and asphalt volumes, appears to be range bound at the 1.15 to 1.33 million (seasonally adjusted) level for 2018 and 2019.

For comparison purposes, the U.S. averaged 1.58 million annual starts from 1970 to 2007. As a result, the median age of housing stock is increasing, growing from an average of 25 years old in 1989 to 40 years old in 2019, according to Toll Brothers.

This is creating strong pent-up demand for housing in the U.S., particularly as the number of households across the nation continues to grow.

Interest rates, a key driver of housing starts, have also declined more than 100 basis points since Jan. 1. This may reinvigorate the housing market in the second half of 2019 and into 2020.

On highway funding

Despite the lack of a federal infrastructure bill, the U.S. infrastructure market is stronger than it has been in more than a decade.

State and local infrastructure spending, which often accounts for two-thirds or more of overall infrastructure spending in the U.S., exceeded $300 billion annually (seasonally adjusted) for the first time in April. With numerous state and local infrastructure spending bills driving increased spending, the market will likely improve even if the FAST Act expires in October 2020 and federal spending is held at current levels.

The wild card of an infrastructure package, which appears to be one of the few areas of potential agreement between the two major parties, may increase in probability in the event a recession does rear its head over the next two years.

Final thoughts

In short, while the specter of a recession appears to be hanging over the market, the fundamentals of the U.S. construction materials market remain strong.

FMI anticipates continued growth in the sector in the second half of 2019 and into 2020. However, improvements in profitability among public companies will be needed to drive an increase in M&A transaction closings. A return to more normal weather patterns would go a long way to make this a reality.

Until then, the market for transactions will continue to be dominated by small to mid-sized transactions that hold ample synergies for acquirers.

George Reddin and Scott Duncan are managing directors with FMI Capital Advisors Inc., FMI Corp.’s investment banking subsidiary. They specialize in mergers and acquisitions and financial advisory services.

Subscribe to Pit & Quarry

If you enjoyed this article, subscribe to Pit & Quarry to receive more articles just like it.

1 Comment on "The latest merger & acquisition influencers"

Trackback | Comments RSS Feed

Inbound Links