Aggregate Forecast: The V-shaped recovery continues

The construction market is experiencing growth in the residential segment. Click to enlarge. Source: SC Market Analytics

We should know very soon who won the election, right?

Well, no matter, what we do get is a great civics lesson.

The outlook is little changed from last month, when we called for a rapid recovery in residential activity. We can add manufacturing to that as the V-shaped recovery continues. With the $3 trillion stimulus that’s making its way through the economy and interest rates at record lows, the field is set for above 4 percent GDP growth over the next six months.

All the uncertainties (i.e., COVID, the election) are getting closer to being resolved. Soon, the conversation will shift to massive debt loads and how to slow the growing debt/GDP ratio. Not much will be done, though, because it is too painful for anyone to enact remedies such as a balanced budget.

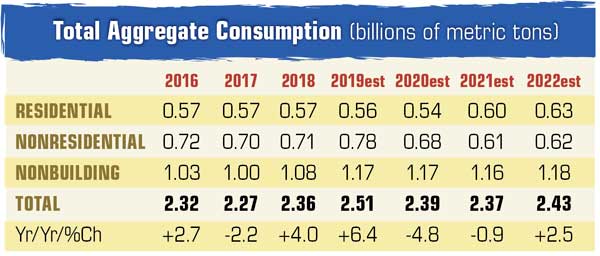

Residential

Construction-wise, growth is fantastic in the residential segment. More jobs are added, and mortgage rates remain extremely low.

Nonresidential

Nonresidential will not rebound anytime soon (expect that post-2022 when higher demand shows up). The COVID lockdowns accelerated the Amazon effect, and some of the changes will become structural (i.e., less density and more online shopping) for a decade.

Nonbuilding

Infrastructure is more complex. Everyone talks about new infrastructure stimulus, but the definition of “infrastructure” keeps changing. Now, it means more than roads and bridges; it also means electric grid, energy alternatives, electric charging stations, education and more. This means any new infrastructure funds will be spread out and less concentrated in roads and bridges.

In addition, the state and local budgets will take a few years to return to health. As a result, we see modest, uneven gains in aggregate going into infrastructure – higher, but not by much.

By region

Regionally, the states that have shut down the most and the longest will take the longest to recover, as some businesses have left and the new ones replacing the old will take a little time to get going.

This means the Southeast, Mountain states and Midwest will grow the fastest.

Aggregate pricing strength will return by mid-2021 in most areas.

David Chereb, Ph.D., is with SC Market Analytics (SC-MA), which produces customized market forecasts by major segment of construction, from the county level up. Clients use SC-MA market intelligence reports for business planning and acquisition analyses in aggregate, ready-mixed concrete and cement. For more information, visit sc-marketanalytics.com.

Featured photo: P&Q Staff

Subscribe to Pit & Quarry

If you enjoyed this article, subscribe to Pit & Quarry to receive more articles just like it.